GST In Malaysia Explained

Types of GST

There will be three different categories of goods & services under the GST scheme in Malaysia. They are:

I. Standard-Rated GST

Goods and services in this category will be charged a tax rate of 6% at every stage of the supply chain. The tax is billed and collected by businesses and paid to the government. Every party except the final consumer can claim back credits on the GST they already paid (known as input tax). Examples of the goods in this category are cloth, car and fruits. The following diagram shows how Standard-Rated GST works:

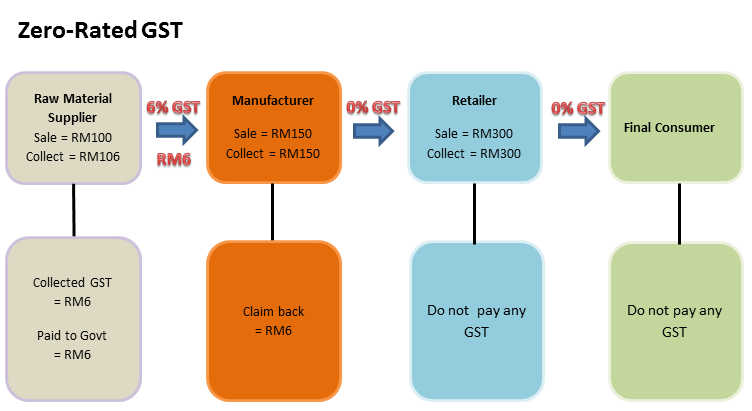

II.Zero-Rated GST

Goods and services in this category will be charged a GST rate of 0%. This means that GST is not charged to the final consumer. But businesses CAN claim back credits on their input tax. Examples of goods in this category are basic food item (meats, fish and cooking oil) and first 200 unit of electricity per month. The following diagram shows how zero-rated GST works, assuming the final product is zero-rated but the raw materials are standard rated:

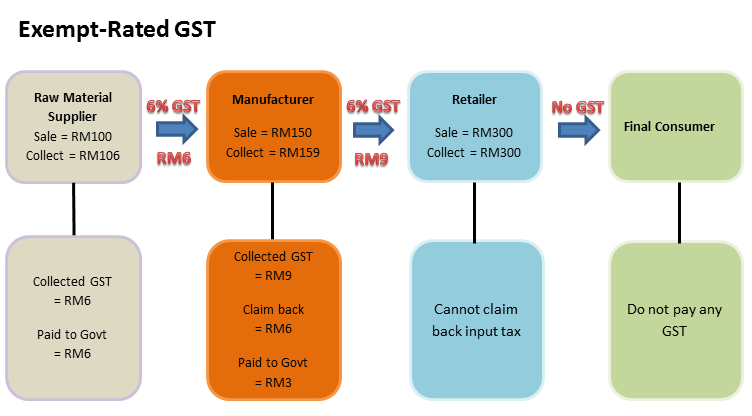

III.Exempt-Rated GST

Goods and services that fall in this category will be non-taxable and are not subject to GST at the output stage. This means that GST is not charged to the final consumer. But it also means that businesses, particularly the final party in the supply chain (before the final consumer) CANNOT claim back credits on their input tax even if they might have incurred it earlier on. Examples of goods in this category are residential property and health care services. The following diagram will give a clearer picture on how Exempt-Rated GST works:

– See more at: http://www.qne.com.my/